Offshoring prosperity

Agroholdings and tax avoidance in Ukraine

Alexander Kravchuk and Mykhailo Neboha with Julie de los Reyes

This article is the second in a weekly series of three special edition longreads focusing on rural-urban inequalities in Ukraine. It is the outcome of a collaboration between TNI and the Commons: Journal of Social Criticism – an independent, internationally minded and progressive online and print journal from the Ukraine, publishing articles, interviews, reports, blogs and opinion pieces on current affairs in the Ukrainian, Russian and English languages.

![]()

Since independence, agriculture has been positioned as Ukraine’s economic engine. The country benefits from a favourable climate and is endowed with one of the world’s most fertile agricultural soils: the so-called ‘Black Earth’. Over a third of its total land area is agricultural land, of which 56 per cent is arable land — one of the highest in Europe. In recent years, it has earned the title “breadbasket of the world”, a recognition of its importance as a major agricultural supplier globally. Ukraine now stands as the third largest exporter of grain after the United States and the European Union, supplying 12 per cent of the world grain market. It ranks 6th place in the global wheat trade, 4th in corn trade, and 1st in sunflower oil trade.

The economic roadmap followed by Ukraine over the past decades re-oriented production towards (mainly Western) export markets and favoured the growth of an agro-industrial sector. While often touted as a success story, this developmental path had limited spillover effects in the rest of the economy and did not lead to broad-based, inclusive and sustainable growth. A combination of flawed state policy and neoliberal reforms resulted in the gains being highly skewed in favour of agroholding companies — horizontally and vertically integrated export-oriented firms that dominate agricultural production and trade. As much as 29 per cent of agrarian land are under the control of agroholdings, up from 8 per cent in 2007, and about 22 per cent of total agricultural output flows through these firms.

Agroholdings

Agroholdings refer to large-scale farming enterprises with at least ten thousand hectares (ha) of land under management. They are an agglomeration of multiple farms and enterprises, often organisationally structured as a parent entity with control over subsidiary firms or corporate farms – what is also sometimes referred to as ‘Large Farm Management’ (LFM). There are 93 such LFM enterprises in Ukraine, each controlling over 10,000 ha. The average size of an agricultural enterprise forming part of an agroholding is 4,850 ha. Agroholdings are strongly associated with the type of large-scale farming that emerged in former Soviet states like Russia, Ukraine, and Kazakhstan. While the average farm size in Ukraine is 1,058 hectares, it is not unusual for farm sizes to reach up to 600,000 ha. This compares to an EU farm size average of 16,1 ha.

In this article, we first consider the rise of agroholdings as part of the broader transformation of Ukraine´s agricultural sector after 1991, in the wake of the dissolution of the former Soviet Union. The restructuring that followed sought to dismantle the structures of the old Soviet regime in favour of the world market system, and with it, a dramatic shift in the rules on land ownership, agricultural price formation, competition, and trade. Agroholding companies emerged as the preferred model for organising production on a large scale and for spearheading the state’s rural development strategy. We highlight the socio-economic implications and some of the problems associated with their operations.

Secondly, we take a closer look at the economic contribution of the agricultural sector. Relative to its size and compared to other sectors, agriculture’s share is small, contributing to about 10 to 12 per cent of GDP.1 Whilst this is partly due to the low added value of agricultural produce, exposure to price volatility in commodity markets, preferential treatment given to large agribusinesses, and the ‘shadow cultivation’ of land undercut the expected gains. This raises questions on the effectiveness of current state policy to harness agriculture’s potential not only as a driver of economic growth but to address rural poverty and inequality.

Finally, we look at some of the ways through which agroholding companies have been able to preserve their position within the agricultural sector. Tax avoidance and offshoring are common practices among the sector’s largest firms, allowing them to accumulate very large profits abroad. We focus on the case of offshoring in corn to illustrate the scale of financial outflows associated with these schemes.

From collective farming to agroholdings

Ukraine has a long agrarian history, with significant changes over time in the nature of its production systems. It was once the breadbasket of the former Soviet Union to which, as a constituent republic, it supplied key agricultural produce like wheat. In 1991, the country underwent a protracted period of transition into a market economy, progressively opening up key sectors to private ownership and foreign investment. In agriculture, economic reform has led to the privatisation of farmland, supplanting ‘collectivisation’ arrangements under Soviet times. The collective farms, state owned farms and household farms were privatised into smallholder farms, with land titles allocated to small plots, while at the same time withholding the free purchase and sale of land. The re-organisation of land ownership and labour was meant to incentivise small-scale farming and transform the rural countryside. Instead, it led to the consolidation of land in the hands of rural elites, and subsequently, in the emergence of an agricultural system based on land lease, and a new form of agribusiness organisation dominated by agroholdings.

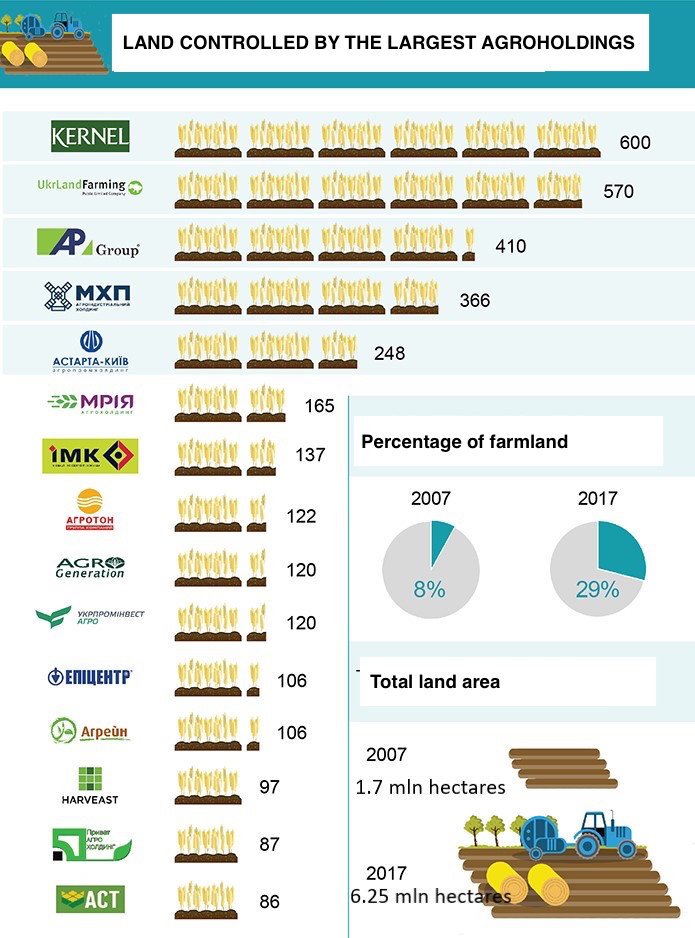

Absent state support and incentives for small farmers to cultivate their own land, land certificates were leased collectively to large farms at a low cost. It is estimated that 99 per cent of the land rented out is from private households that mainly depend on lease contracts as a source of income. While ownership remains in the hands of smallholders, the use of land is firmly under the control of agroholdings. Indeed, with an estimated 2.8 million ha now concentrated in the ten largest firms (see Figure 1), the Ukrainian countryside is marked by extreme levels of land concentration.

Figure 1. Ukraine’s largest agroholding firms and land area cultivated, in thousand hectares

Source: AgroPortal

The dominance of agroholding companies has implications not only for the concentration of land but also of capital and labour under their management. In contrast to small and medium enterprises, agroholdings enjoy access to international capital markets and international financial institutions which help them undercut or absorb smaller competitors, thereby locking out alternative types of farms and farming. Stock listings in the financial centres of London, Warsaw, and New York, as well as financing from the World Bank’s International Finance Corporation (IFC), the European Bank for Reconstruction and Development (EBRD) and export credit agencies have helped build and reinforce the position of agroholdings in the agricultural sector. Large-scale, corporate farming is also capital intensive, tends to employ mechanisation as a substitute for labour, and favours specialisation in a few crops. This contributes to increasing unemployment in the countryside as well as fluctuations in labour demand, which has to correspond to the seasonality of mono-cropping and crop specialisation. Beyond crop production, employment opportunities have also become even more limited given the low diversification in economic activity in rural areas.

Agroholdings have been implicated in issues of environmental degradation and soil depletion. The crop mix and rotation they require have negatively impacted soil fertility, as they tend to focus on valuable and fast-paying cash-crops destined for export markets. Sunflower, maize and soya are three of the main crops grown by these companies, some of which were cultivated as monocultures due to their high profitability.2 The largest agroholding firms like Kernel, IMC, MHP and Astarta allotted between 50 to 84 per cent of their land to these crops.

Volatility, preferential treatment and shadow cultivation

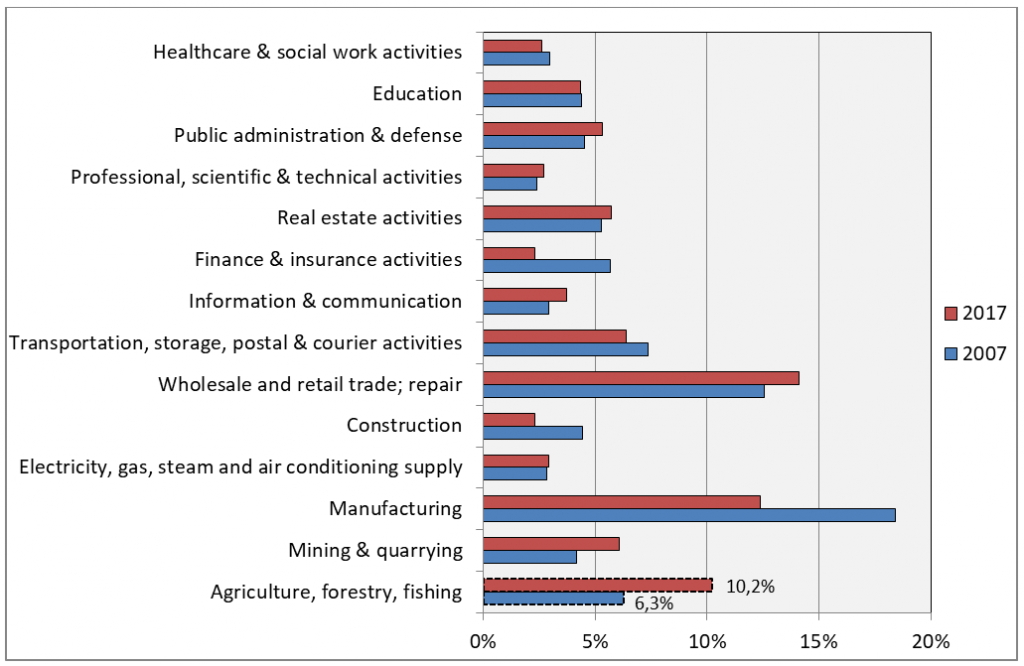

Agriculture’s share in Ukraine’s GDP has steadily increased over the years, from 6.3 per cent in 2007 to 10.2 per cent in 2017 (see Figure 2). Its share in the country’s exports is equally on the rise: crop production accounted for 32 per cent in 2017, up from 19.7 per cent just 6 years ago, with exports in physical volume increasing from 50 per cent to 80 per cent. The sector’s share in employment is also significant: despite the automation and mechanisation of agricultural production, more than 2.8 million people remain employed, or 18 per cent of the total Ukrainian workforce in 2017. This makes agriculture one of the most important and fastest growing sectors of the Ukrainian economy.

Figure 2. Sectoral structure of Ukraine’s economy and sectoral contribution to GDP, 2007 and 2017

Source: Based on data from the State Statistics Service of Ukraine.

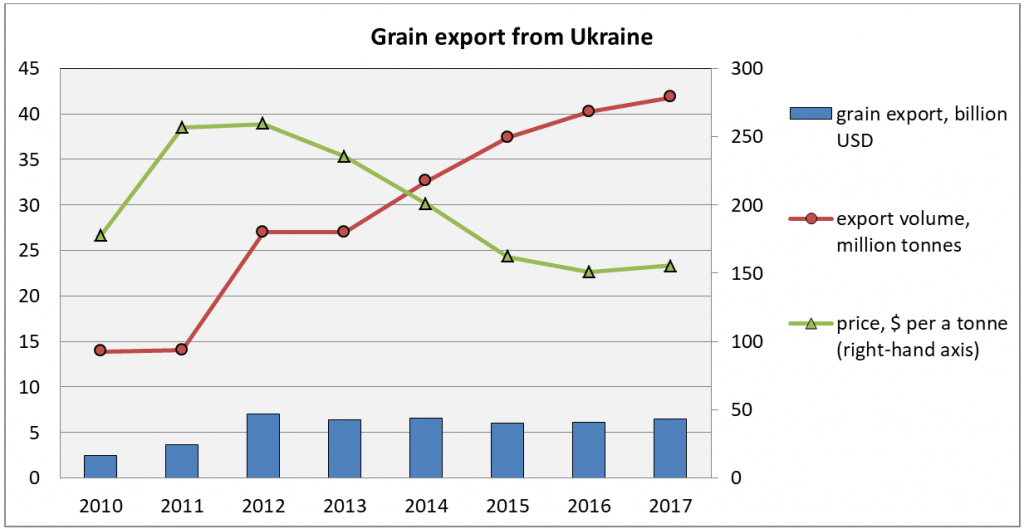

Yet, despite these numbers, agriculture’s share in the country’s GDP remains relatively modest. While this is partly explained by the peculiarities of the agricultural sector—where products have lower value added compared, for instance, to industrial products—this value added is further diminished by a host of other problems. Firstly, the agricultural sector is highly vulnerable to volatility in global commodity markets. Figure 3 shows how even an increase in the volume of grain exports to 42 million tonnes a year does not significantly increase the volume of foreign currency inflows into Ukraine since the average price for such products has halved to $155 per tonne. In contrast to the price fixing of agricultural produce, set at above world market prices during Soviet times, the international price system fluctuates freely and is much harder to predict. This renders countries and sectors that are export-oriented especially susceptible to sharp swings in revenues and foreign exchange earnings.

Figure 3. Export of grain from Ukraine in physical and monetary terms, 2010 to 2017

Source: Based on data from the National Bank of Ukraine.

Secondly, agriculture, being the flagship sector of the economy, enjoys preferential treatment. This is most evident in the state’s taxation policy. Agricultural producers 3are exempt from income tax and, up until 2016, benefitted from a special VAT regime. They are only required to pay a fixed tax rate (linked to a normative monetary evaluation of land that for a long time has not been adequately reviewed) and were exempted from paying VAT as well as taxes on profits and land and fees for water. While preferential treatment is not problematic per se, the current tax regime unduly benefits the largest enterprises. This was made even more apparent in 2016 and 2017, when direct state subsidies were given to large producers to offset the effects of the abolishment of the preferential treatment. In 2017 for example, about half of the entire subsidy (UAH 2 billion) went to the enterprises of the Myronivsky Hliboproduct group, which belonged to oligarch Yuriy Kosyuk. The country’s oligarchs are well positioned to lobby for favourable terms such as VAT refunds whereas small producers generally do not have access to the VAT refunds since they are not registered as taxpayers. Moreover, preferential treatment for the largest firms contradicts the government’s rhetoric about supporting small and medium-sized enterprises and stimulating market competition.

Finally, the ‘shadow cultivation’ of agricultural land, whereby state-owned land is used for illicit trafficking and is transferred to private companies, presents another pressing problem within the sector. Ukraine has 42.7 million ha of agricultural land, of which 25 per cent are held by the state. In recent years, numerous cases have been uncovered involving state officials illegally allocating land for private use. Such transactions are ‘off the books’, allowing private companies to cultivate the land while evading the single land tax. Preliminary estimates by the National Anti-Corruption Agency suggest that the damage from this scheme exceeds UAH 2 billion or USD 71.5 million. High profile cases have included one of the largest players in the agricultural market, PJSC State Food Grain Corporation, which has been cited for falsifying trading accounts and grand theft.

Tax avoidance and offshoring

The liberalisation of the economy, an essential tenet of Ukraine’s transformation from command to free market management, brought with it new opportunities for accumulation by the capitalist class. The lifting of barriers to trade was intended to harness Ukraine’s export potential and facilitate its integration in global markets, a policy pushed for by western creditors and international institutions like the IMF as a condition for extending credit to the country. Large agribusinesses specialising in the export of grains, oilseeds, fats and oils have been one of the main beneficiaries of this opening up.

Liberalisation, however, also served as the precondition for the exodus of domestic capital as it opened up access to tax havens, offshore accounts and financial services abroad. Compounded by existing loopholes in the state’s tax regime, a ‘shadow market’ in grain production and trade emerged, leading to billions of dollars in yearly losses to the national budget. The shadow market includes such practices as the setting up of offshore companies to avoid taxation, the understatement of production and trade volumes to lower the taxable base, and the illegal transfer of state-owned land into private hands. Estimates suggest that Ukraine’s shadow market constitutes between 40 to 45 per cent of its GDP in 2015, and up to 40 per cent of its grain market.4 Offshoring, in particular, is responsible for about 100 to 150 billion UAH in lost revenues a year, making it the primary scheme through which significant contributions to the state coffers are lost.

Offshoring occurs when a firm sets up or registers as an as offshore entity in countries with a lower tax base and more permissive regulatory environment than their home countries. While technically legal, it permits companies “to do things they can’t do otherwise” onshore. In Ukraine, offshore jurisdictions have been widely used by the largest corporations to siphon off earnings and profits. According to the figures of the State Fiscal Service of Ukraine, about two thirds of export operations in Ukraine are processed through offshore entities. All agroholding companies operate as offshore legal entities.

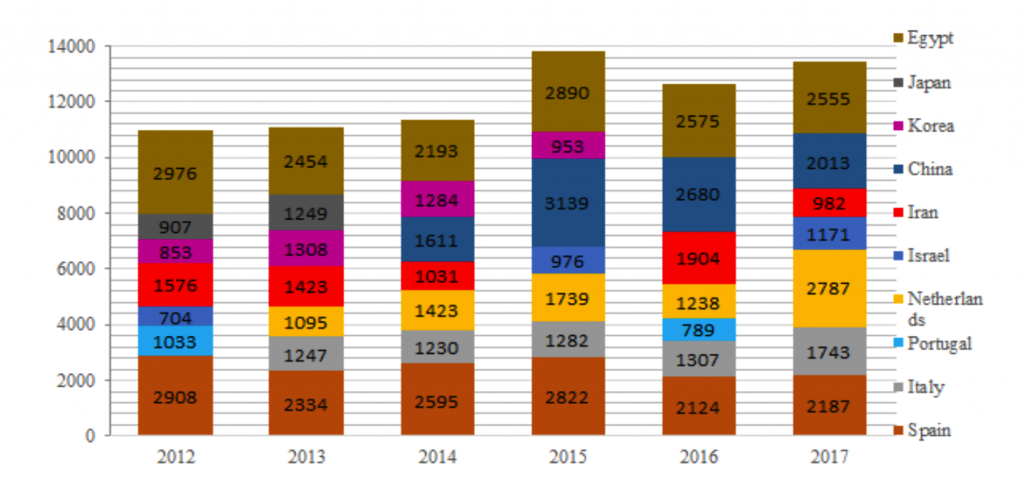

Looking at the example of corn, which accounts for the largest share in Ukrainian crop exports, helps illustrate the extent of financial outflow from offshoring. The export of corn is concentrated in five countries—Spain, Italy, the Netherlands, Egypt and Iran—which together make up 50 per cent of total corn exports (see Figure 4). Direct exports from Ukraine to these countries only stand at 1 to 2 per cent, whereas 98 to 99 per cent come from companies ‘residing’ (i.e. registered) in other countries, like Switzerland, Cyprus, Virgin Islands, Great Britain, Panama and UAE—some of the world’s major tax havens (see Figure 5). Almost the entire trade in corn is routed through ‘transit’ countries on paper, even as the physical goods are directly delivered to the destination countries, where the goods are consumed. The only exception is the Netherlands, which imported 18 per cent of corn directly, although this is heavily influenced by the country’s status as a tax haven.

Note on methodology

The Ukrainian customs databases and open sources such as YouControl have been used to establish actual contract chains and destination countries in the export of grains, and for information on supply chains, importers, amounts and prices. The analysis was carried out using the example of corn exports which accounts for the largest share in Ukrainian crop exports.

Figure 4. Destination of corn exports from Ukraine, 2012 to 2017, in thousand tonnes

Source: Own calculations

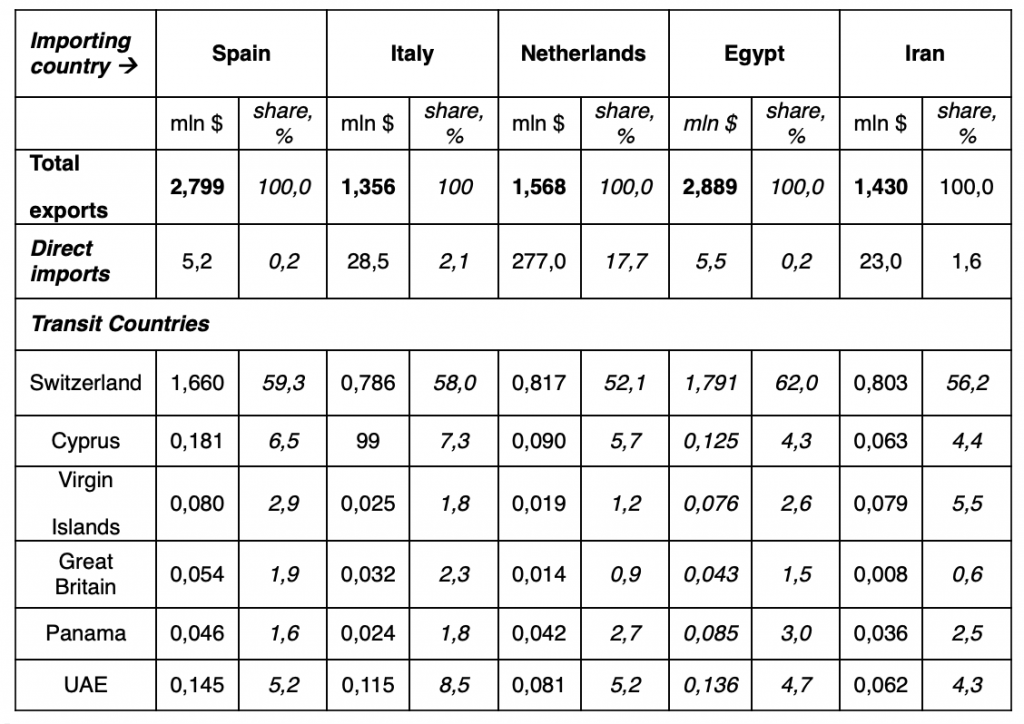

Figure 5. Corn supply channels to the main importers, 2012-2017.

Source: Own calculations

Explanation of figure: Using the example of the first column. The total Ukrainian exports of corn to Spain amounted to 2,799 million USD (or 2.8 billion USD) between 2012 – 2017. However, according to customs data, Spain received only 5,2 million worth of corn from Ukraine directly, just 0,2% of the total value. Most of the actual supply was carried out off-shore, through various transit countries e.g. 59% of the total corn exports from Ukraine to Spain transited through Switzerland (amounting to 1.660 million USD), 6,5% via Cyprus (amounting to 0,181 million USD) etc.

The purpose of trading through transit countries is to avoid or minimise taxes on income, in this case accomplished by understating corn export prices. On average, 1 ton of corn allowed each exporter to ‘offshore’ between 10 to 20 US dollars. Taking into account the export volumes from 2012 to 2017 (inclusive), the overall amount of funds transferred from Ukraine reaches 1.2 billion US dollars (26 billion UAH) in corn exports alone. Thus, a considerable amount of income remains in the accounts of companies related to exporters in these countries. Companies registered in Switzerland are the absolute leaders within this offshore transit trade, having shipped 53 per cent of the grain.

The example of corn is not an isolated case, but rather reflects the broader trend in grain exports. As one study also revealed, as much as 43 per cent of Ukrainian export of goods in 2014 was trans-shipped through eight countries including the Virgin Islands, Cyprus, Panama and Switzerland, whereas only 2.41 per cent of goods were consumed in these countries. Considering that the 2012-2017 exports of wheat, corn, soybeans, rapeseeds and sunflower oil are worth 65 billion USD, the approximate amount of funds moved from Ukraine stands at about 4.5 billion USD – a huge sum that a debtor country like Ukraine could have used to pay off its debts or to re-invest in the domestic economy.

بـ. عودة العلاقات الرسمية مع الكيان الصهيوني

Ukraine’s international success as an agricultural powerhouse belies the problems that the sector faces internally. The current model for organising agricultural production has resulted in increasing inequality in the rural areas rather than promoting self-sufficiency and food security. Agroholdings dominate, buoyed up by subsidies, preferential treatment, and access to international markets. The impact of their operations on land, labour, and the environment put into question the desirability of this organisational form in relation to other types of farming arrangements and practices.

In terms of economic contribution, while the agricultural sector has become a leader in the Ukrainian economy both in terms of production volumes and exports, preferential treatment and other state support given to agricultural producers limit its contribution to the state budget. Moreover, tax breaks and direct subsidies only serve to provide untaxed enrichment to the largest companies and comes at the expense of broader development goals. The same companies are also at the forefront of large-scale tax avoidance, which further erodes the potential gains from the sector. Closing down legal loopholes should be a priority to immediately stem the huge capital outflows associated with these schemes.

Fundamentally, Ukraine needs to reconsider the development trajectory that it has followed since independence as its failings have become increasingly apparent. The type of agriculture and rural development that it pursues—through state policy, market regulations, tax regimes, and economic incentives—have so far prioritised the economic interests of the few at the expense of environmental sustainability, food sovereignty, and rural vitality. A new rural paradigm is needed that will lead to a healthy, multifunctional agricultural system.

نبذة عن الكاتب/ة

Alexander Kravchuk: Ph.D. in Economics, member of the editorial board of the Commons: Journal of Social Criticism, analyst at the Center for Social and Labor Research. Email: akravchuk2@gmail.com

Mykhailo Neboha: Ph.D. in Economics, economist, independent researcher on offshore schemes in Ukraine. Email: neboga@ukr.net

Julie de los Reyes: Ph.D in Geography, University of Manchester. Email: j.delosreyes@tni.org