Obsessed with Numbers A Critical Analysis of the United Nations’ Crop Monitoring Programme in Peru, Colombia and Bolivia Nicolas Martínez and Pien Metaal. Translator: Analia Penchaszadeh

Ruling the Waves How corporations are deepening their control of global ocean politics Carsten Pedersen (TNI) and Dr. Felix Mallin (University of Copenhagen)

Land rights and wrongs What role does land titling play in helping coca leaf farmers switch to legal alternatives in Colombia? Sophia Ostler

A House of Cards ‘High compliance’: A legally indefensible and confusing distraction A Commentary by Martin Jelsma (TNI), David Bewley-Taylor (GDPO), Tom Blickman (TNI), and John Walsh (WOLA)

‘Caring Communities for Radical Change’ Debates and future directions on degrowth from the 8th International Degrowth Conference – A reportage Daniel Boston

In search of Real Utopias The Transformative Cities People’s Choice Award as a research tool Erick Palomares

Generals to the dustbin, Algeria will be independent The New Algerian Revolution as a Fanonian moment Hamza Hamouchene

How Seaspiracy misses the big picture Mads Barbesgaard, Zoe Brent, Carsten Pedersen and Daniel Boston

The Transformative Cities People’s Choice Award and the Atlas Of Utopias Introduction to a process-platform to facilitate the transition to a post-capitalist world Sol Trumbo Vila

Algorithmic assembly lines Digitalization and resistance in the retail sector Janina Hirth and Markus Rhein

COVAX: A global multistakeholder group that poses political and health risks to developing countries and multilateralism Harris Gleckman

De vervuiler is koning Het falen van de vrije energiemarkt in Nederland Jilles Mast en Lavinia Steinfort

Taking on the Tech Titans Reclaiming our data commons Ben Hayes, Ben Tarnoff, Vahini Naidu, Anita Gurumurthy, Caroline Nevejan, Nanjira Sambuli

Juggling crises Latin America's battle with COVID-19 hampered by investment arbitration cases Cecilia Olivet and Bettina Müller, Transnational Institute

Feminist Realities Transforming democracy in times of crisis Tithi Bhattacharya, Awino Okech, Khara Jabola-Carolus, Laura Roth and Felogene Anumo

States of Control The dark side of pandemic politics Fionnuala Ni Aolain, Arun Kundnani, Anuradha Chenoy and María Paz Canales

Taking Health back from Corporations Pandemics, big pharma and privatized health Susan George, Baba Aye, Mark Heywood, Kajal Bhardwaj and David Legge

A Recipe for Disaster Food systems, inequality and COVID-19 Rob Wallace, Moayyad Bsharat, Arie Kurniawaty, Sai Sam Kham and Paula Gioia

Agroecology and Food Sovereignty The Role of Small-Scale Fishing Cooperatives in the Istanbul Region Irmak Ertör

Gender and Fisheries in Indonesia Solidaritas Perempuan Anging Mammiri South Sulawesi & Transnational Institute

Looking in the Mexican Mirror 26 years of free trade: industrial paradise for transnational corporations and environmental hell for the people Mónica Vargas (Transnational Institute)

Cashing in on the Pandemic How lawyers are preparing to sue states over COVID-19 response measures Corporate Europe Observatory & Transnational Institute

Pandemic Profiteers How foreign investors could make billions from crisis measures Cecilia Olivet, Lucia Bárcena, Bettina Mueller, Luciana Ghiotto and Sara Murawski

The Uruguayan Left at the Crossroads Notes for progressives in Latin America and the world Daniel Chavez

In and against the European Union? The Portuguese experience of an anti-austerity government in the EU, and its relevance to the UK Hilary Wainwright

A Living Countryside The land politics behind the Dutch agroecology movement Jeannette Oppedijk van Veen, Leonardo van den Berg, Sijtse Jan RoeteJolke de Moel, Hanny van Geel (all members of Dutch farmers organisation "Toekomstboeren")

Gender dan Perikanan di Indonesia Solidaritas Perempuan Anging Mammiri South Sulawesi & Transnational Institute

Offshoring prosperity Agroholdings and tax avoidance in Ukraine Alexander Kravchuk and Mykhailo Neboha with Julie de los Reyes

Sentinels of Privilege and the Ressentiment of the Powerful The New Right in Brazil Rita de Cácia Oenning da Silva and Kurt Shaw

End of a golden age? Progessive governments and post-neoliberalism in Latin America Franck Gaudichaud interviews Miriam Lang and Edgardo Lander

The longterm crisis The Venezuelan oil rentier model and the present crisis the country faces Edgardo Lander

La obsesión por las cifras Análisis crítico sobre el Sistema de Monitoreo de Cultivos de las Naciones Unidas en Perú, Colombia y Bolivia Nicolas Martínez y Pien Metaal

Gobernar las olas El control empresarial de la política mundial de los océanos Carsten Pedersen (TNI) y Dr. Felix Mallin (Universidad de Copenhague)

Los derechos y reveses de la tierra La titulación de la tierra como mecanismo para el desarrollo alternativo en Colombia Sophia Ostler

Erradicación Manual Forzosa Otro revés para el estado y los derechos de las comunidades Ricardo Vargas M (Corporación Viso Mutop)

In search of Real Utopias The Transformative Cities People’s Choice Award as a research tool Erick Palomares

Generals to the dustbin, Algeria will be independent The New Algerian Revolution as a Fanonian moment Hamza Hamouchene

The Transformative Cities People’s Choice Award and the Atlas Of Utopias Introduction to a process-platform to facilitate the transition to a post-capitalist world Sol Trumbo Vila

COVAX: A global multistakeholder group that poses political and health risks to developing countries and multilateralism Harris Gleckman

Juggling crises Latin America's battle with COVID-19 hampered by investment arbitration cases Cecilia Olivet and Bettina Müller, Transnational Institute

Feminist Realities Transforming democracy in times of crisis Tithi Bhattacharya, Awino Okech, Khara Jabola-Carolus, Laura Roth and Felogene Anumo

Looking in the Mexican Mirror 26 years of free trade: industrial paradise for transnational corporations and environmental hell for the people Mónica Vargas (Transnational Institute)

Cashing in on the Pandemic How lawyers are preparing to sue states over COVID-19 response measures Corporate Europe Observatory & Transnational Institute

Pandemic Profiteers How foreign investors could make billions from crisis measures Cecilia Olivet, Lucia Bárcena, Bettina Mueller, Luciana Ghiotto and Sara Murawski

The Uruguayan Left at the Crossroads Notes for progressives in Latin America and the world Daniel Chavez

End of a golden age? Progessive governments and post-neoliberalism in Latin America Franck Gaudichaud interviews Miriam Lang and Edgardo Lander

The longterm crisis The Venezuelan oil rentier model and the present crisis the country faces Edgardo Lander

Transnational Institute2021-05-17T12:01:56+02:00 STATE OF POWER 2020 Charming Psycopaths The modern corporation An interview with Joel Bakan

Transnational Institute2021-05-17T12:02:06+02:00 STATE OF POWER 2020 The Intelligent Corporation Data and the digital economy Anita Gurumurthy & Nandini Chami

Transnational Institute2021-05-17T12:02:14+02:00 STATE OF POWER 2020 Beyond China, Inc. Understanding Chinese companies Lee Jones

Transnational Institute2021-05-17T12:02:27+02:00 STATE OF POWER 2020 The Corporate Architecture of Impunity Lex Mercatoria, market authoritarianism and popular resistance Adoración Guamán

Transnational Institute2021-05-17T12:02:34+02:00 STATE OF POWER 2020 Corporations as Private Sovereign Powers The case of Total Alain Deneault

Transnational Institute2021-05-17T12:02:46+02:00 STATE OF POWER 2020 The Financialised Firm How finance fuels and transforms today’s corporation Myriam Vander Stichele

Transnational Institute2021-05-17T12:02:52+02:00 STATE OF POWER 2020 Touching a nerve How a peoples’ campaign at the United Nations is challenging corporate rule Brid Brennan and Gonzalo Berrón

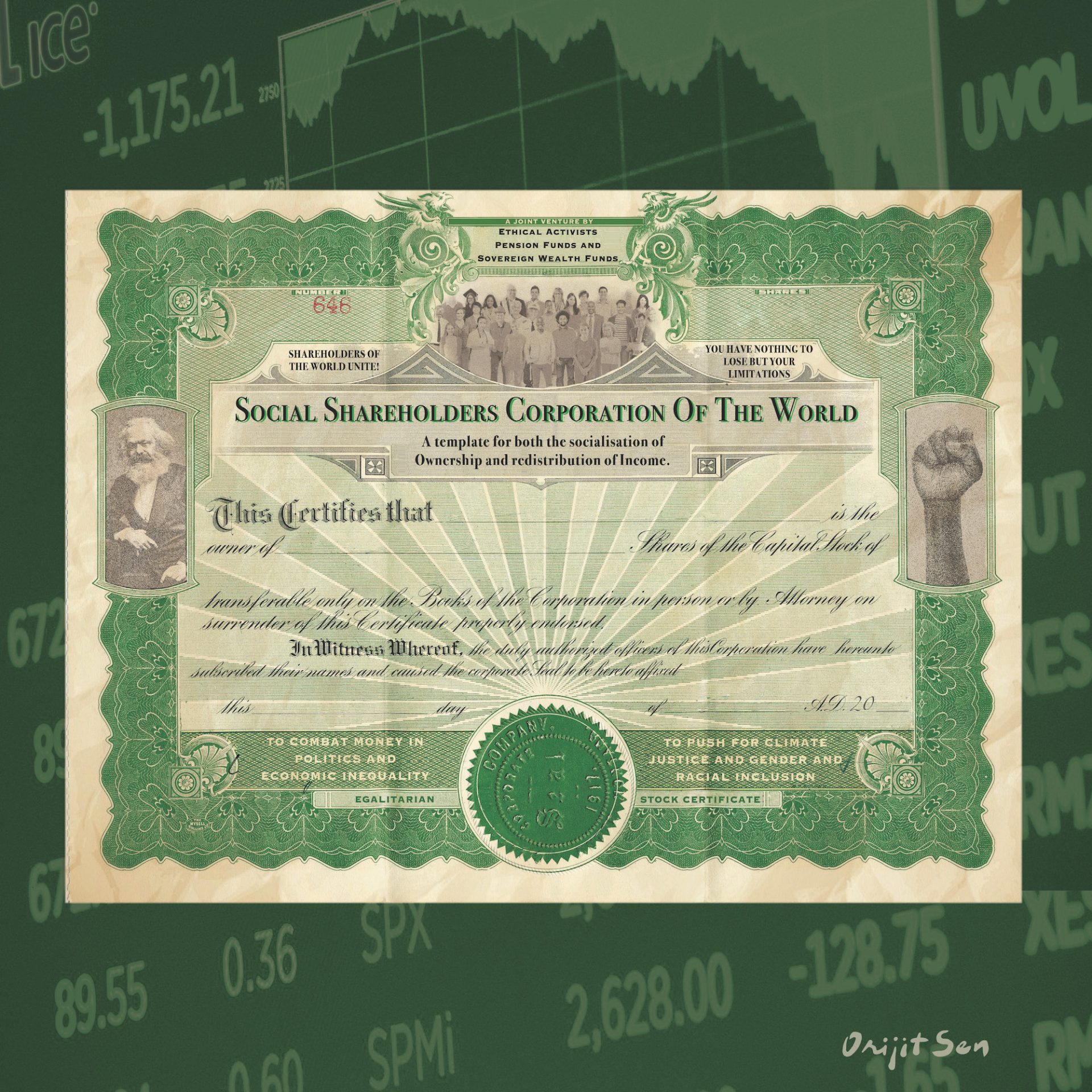

Transnational Institute2021-05-17T12:03:01+02:00 STATE OF POWER 2020 The End of the Corporation? It’s time to make the profit-maximising, shareholder-controlled corporation obsolete Marjorie Kelly

Transnational Institute2021-05-17T12:03:07+02:00 STATE OF POWER 2020 Rethinking the Corporation Conversation with Tchenna Maso, Nomi Prins and Barnaby Francis

Transnational Institute2021-05-17T12:03:12+02:00 STATE OF POWER 2020 Illustrating The Corporation Anastasya Eliseeva

Transnational Institute2021-05-17T12:01:56+02:00 STATE OF POWER 2020 Charming Psycopaths The modern corporation An interview with Joel Bakan

Transnational Institute2021-05-17T12:02:06+02:00 STATE OF POWER 2020 The Intelligent Corporation Data and the digital economy Anita Gurumurthy & Nandini Chami

Transnational Institute2021-05-17T12:02:14+02:00 STATE OF POWER 2020 Beyond China, Inc. Understanding Chinese companies Lee Jones

Transnational Institute2021-05-17T12:02:27+02:00 STATE OF POWER 2020 The Corporate Architecture of Impunity Lex Mercatoria, market authoritarianism and popular resistance Adoración Guamán

Transnational Institute2021-05-17T12:02:46+02:00 STATE OF POWER 2020 The Financialised Firm How finance fuels and transforms today’s corporation Myriam Vander Stichele

Transnational Institute2021-05-17T12:02:52+02:00 STATE OF POWER 2020 Touching a nerve How a peoples’ campaign at the United Nations is challenging corporate rule Brid Brennan and Gonzalo Berrón

Transnational Institute2021-05-17T12:03:01+02:00 STATE OF POWER 2020 The End of the Corporation? It’s time to make the profit-maximising, shareholder-controlled corporation obsolete Marjorie Kelly

Transnational Institute2021-05-17T11:49:31+02:00 STATE OF POWER 2019 Gentrification of Payments Spreading the Digital Financial Net Brett Scott

Transnational Institute2021-05-17T11:49:22+02:00 STATE OF POWER 2019 Finance, Fossil Fuels, and Climate Change Networks of Power in Canada Mark Hudson and Katelyn Friesen

Transnational Institute2021-05-17T11:49:15+02:00 STATE OF POWER 2019 Art, Capital of the Twenty-First Century Aude Launay

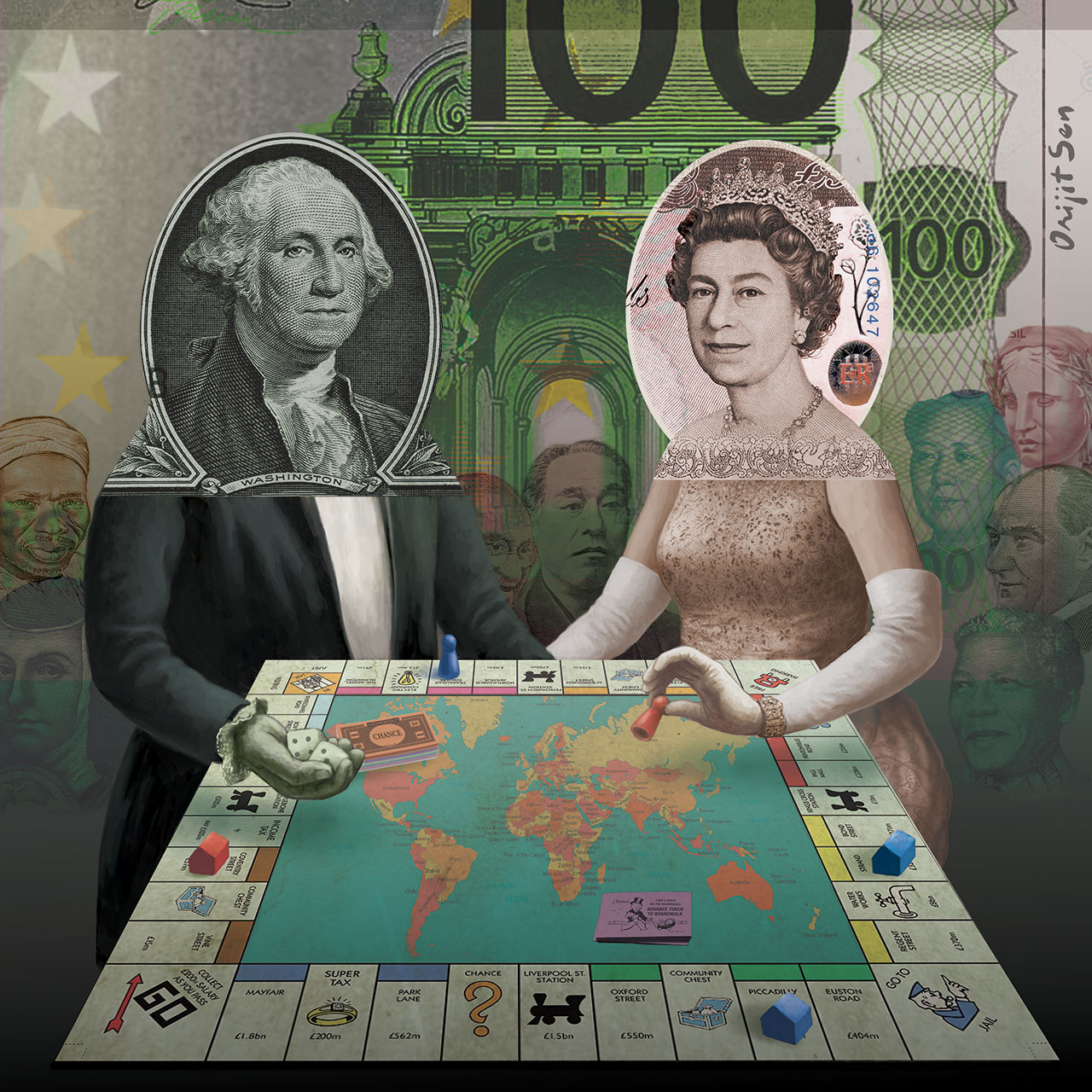

Transnational Institute2021-05-17T11:49:06+02:00 STATE OF POWER 2019 Global Finance Power and Instability Walden Bello

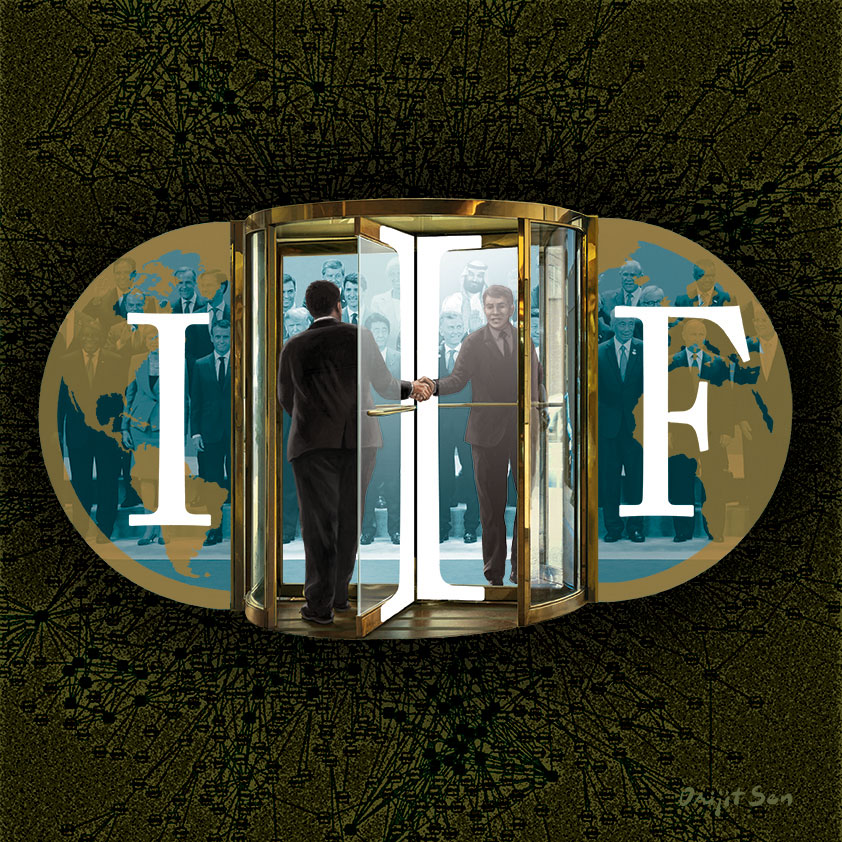

Transnational Institute2021-05-17T11:48:55+02:00 STATE OF POWER 2019 Banking on Public Power Lessons of the Institute of International Finance Jasper Blom

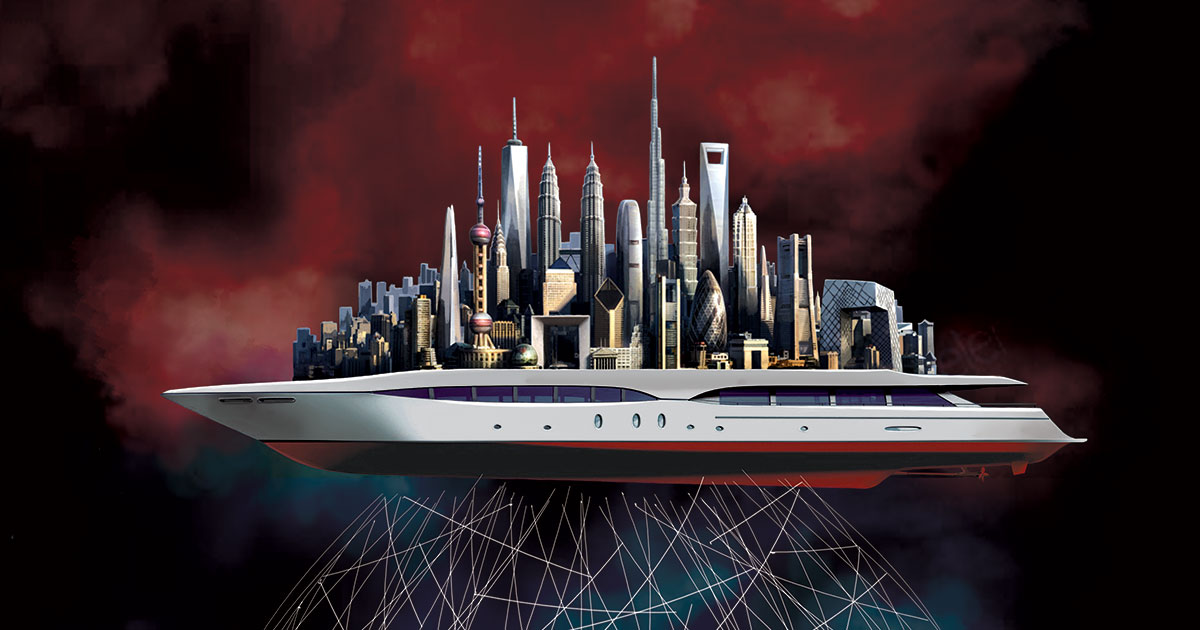

Transnational Institute2021-05-17T11:48:50+02:00 STATE OF POWER 2019 High Finance An Extractive Sector Interview with Saskia Sassen

Transnational Institute2020-11-25T16:46:53+01:00 STATE OF POWER 2019 The Power of Public Finance for the Future we Want Lavinia Steinfort

Transnational Institute2021-05-17T11:48:31+02:00 STATE OF POWER 2019 Offshore Finance How Capital Rules the World Reijer Hendrikse and Rodrigo Fernandez

Transnational Institute2021-05-17T11:48:25+02:00 STATE OF POWER 2019 Battling Bankers Insights on financial power from the grassroots Interview with Simona Levi, Joel Benjamin and Alvin Mosioma

Transnational Institute2020-11-25T16:49:30+01:00 STATE OF POWER 2019 Illustrating Finance Reflections from the State of Power illustrator Orijit Sen

Transnational Institute2021-05-17T11:48:17+02:00 STATE OF POWER 2019 The Latent, Unused Power of Citizens and the Production of Public Collateral Ann Pettifor

longreads2020-10-15T16:50:26+02:00 STATE OF POWER 2018 Marching forward Women, resistance and building counter-power An interview with Bertha Zuniga Caceres, Medha Patkar and Nonhle Mbuthuma

longreads2020-10-15T16:50:06+02:00 STATE OF POWER 2018 Beneath the Pavements, the Beach’ – or the Whirlpool? Lessons of 1968 for building counter-power today Hilary Wainwright

Transnational Institute2020-10-15T16:49:35+02:00 STATE OF POWER 2018 Thinking freedom achieving the impossible collectively Interview with Michael Neocosmos

Transnational Institute2020-10-15T16:49:19+02:00 STATE OF POWER 2018 From Protest Movements to Transformative Politics Luciana Castellina

Transnational Institute2020-10-15T16:49:03+02:00 STATE OF POWER 2018 Without translation, no hay revolución! The importance of interpretation, translation and language justice in building global counter-power Eline Müller and Alice Froidevaux

Transnational Institute2020-10-15T16:48:15+02:00 STATE OF POWER 2018 Building feminist counter-power In for the long haul Nina Power

Transnational Institute2020-10-20T11:16:07+02:00 STATE OF POWER 2018 Flowing movement Building alternative water governance in Mexico Gerardo Alatorre Frenk

Transnational Institute2020-10-20T11:23:19+02:00 STATE OF POWER 2018 Madrid’s Community Gardens Where neighbourhood counter-powers put down roots José Luis Fernández Casadevante Kois, Nerea Morán and Nuria del Viso

Transnational Institute2020-10-20T11:41:18+02:00 STATE OF POWER 2018 People in defence of life and territory Counter-power and self-defence in Latin America Raúl Zibechi

Transnational Institute2020-10-20T11:45:39+02:00 STATE OF POWER 2018 Making counter-power out of madness Laura Flanders

Transnational Institute2020-10-20T11:50:50+02:00 STATE OF POWER 2018 Drawing counter-power Reflections from State of Power illustrator Ammar Abo Bakr

longreads2020-10-20T11:56:16+02:00 STATE OF POWER 2017 Monsters of the Financialized Imagination From Pokémon to Trump Max Haiven

longreads2020-12-08T14:29:15+01:00 STATE OF POWER 2017 All Change or No Change? Culture, Power and Activism in an Unquiet World Martin Kirk, Jason Hickel and Joe Brewer

longreads2020-12-08T14:32:32+01:00 STATE OF POWER 2017 Activism in the Anthropocene Organizing cultures of resilience Kevin Buckland

longreads2024-09-12T10:34:24+02:00 STATE OF POWER 2017 Culture, power and resistance reflections on the ideas of Amilcar Cabral Firoze Manji

longreads2020-10-20T15:17:12+02:00 STATE OF POWER 2017 Power and patriarchy reflections on social change from Bolivia Elizabeth Peredo Beltrán

longreads2020-10-20T16:44:32+02:00 STATE OF POWER 2017 Mall culture and consumerism in the Philippines Jore-Annie Rico and Kim Robert C. de Leon

longreads2021-07-01T11:58:37+02:00 STATE OF POWER 2017 The Media–Technology–Military Industrial Complex Justin Schlosberg

longreads2020-10-27T13:14:47+01:00 STATE OF POWER 2017 The role of human behaviour in generating plutocracies Deniz Kellecioglu

longreads2020-10-27T13:48:59+01:00 STATE OF POWER 2017 White Supremacy as Cultural Cannibalism Gathoni Blessol

longreads2020-10-01T10:59:02+02:00 STATE OF POWER 2017 Gangsters for capitalism why US working class enlists Colin Jenkins

longreads2020-10-20T11:56:16+02:00 STATE OF POWER 2017 Monsters of the Financialized Imagination From Pokémon to Trump Max Haiven

longreads2020-12-08T14:29:15+01:00 STATE OF POWER 2017 All Change or No Change? Culture, Power and Activism in an Unquiet World Martin Kirk, Jason Hickel and Joe Brewer

longreads2020-12-08T14:32:32+01:00 STATE OF POWER 2017 Activism in the Anthropocene Organizing cultures of resilience Kevin Buckland

longreads2020-10-20T15:17:12+02:00 STATE OF POWER 2017 Power and patriarchy reflections on social change from Bolivia Elizabeth Peredo Beltrán

longreads2021-07-01T11:58:37+02:00 STATE OF POWER 2017 The Media–Technology–Military Industrial Complex Justin Schlosberg